Why token buybacks don't work for crypto

Supply, Demand, and the Zero-Sum trap: Why Wall Street's favorite trick fails for web3

A buyback is when a company uses its own funds to repurchase its stocks or tokens from the market. In the stock market, firms often do this to reduce supply and signal confidence to investors

You’ve probably seen announcements like ‘Project XYZ bought back $5M worth of tokens from revenue’ or ‘We’re allocating 80% of revenue to buybacks.’ In fact, token buybacks jumped from $3.3B in 2024 to $8.1B in 2025, a 145% surge. They’re often promoted as a sign of strength, but the data tells a different story.

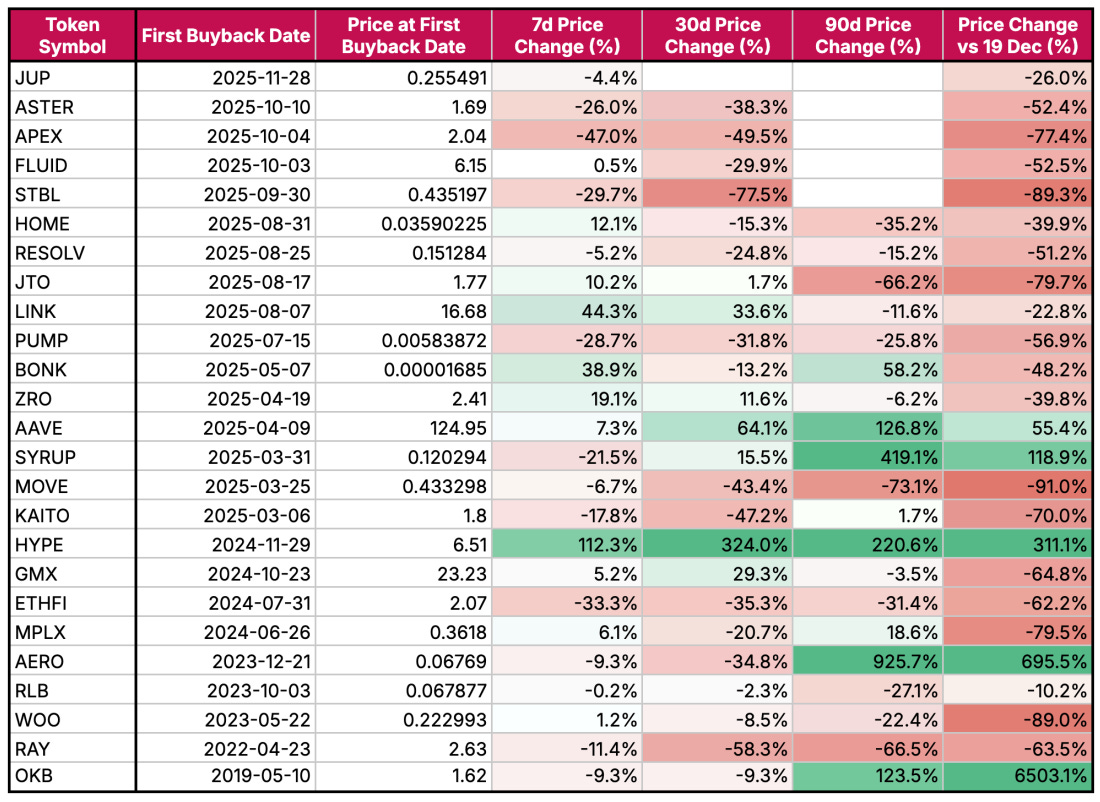

Here is the performance report from Tokenomist 2025 Annual report of major token buybacks. And except for a selected few tokens, the numbers don’t look good for a majority of them.

But you must be wondering, if these projects buy such a huge amount of tokens, why doesn’t it reflect in the token price?

There isn’t just one reason for this, several factors influence token prices even after millions are bought back from the market.

Traditional finance has long relied on buybacks as a way to project strength and reassure investors. Its no surprise that this mechanism became the default choice for many crypto projects as well, to solve the “value accrual” problem.

The narrative was seductive in its simplicity: protocols would generate revenue, use that revenue to purchase their own tokens, thereby reducing the supply and forcing price appreciation through the law of supply and demand. However, if you look at the numbers, there’s a profound disconnect between the promise and the reality.

Here are some main reasons why buybacks don’t really work for crypto in most of the cases.

Protocol Re-pricing

Before we even look into crypto-specific concepts, one must first look into the economic theories and check if they justify them. The prevailing narrative in crypto is that if Demand is the same, and Supply decreases, then the Price must go up. Seems logical, right?

It isn’t. According to modern economists (Modigliani-Miller Theorem), the value of a firm should be determined solely by its underlying assets and earning power, independent of how it finances its operations or distributes its capital. Applied to crypto, a protocol’s total value should be derived from the utility of the protocol and network, its Total Value Locked (TVL), and its fee generating capacity. Whether a protocol chooses to hold its revenue in treasury, distribute it as rewards, or use it to buy back tokens should be irrelevant to the total protocol value.

In digital asset markets, this boils down more into a zero-sum game. When a protocol like Uniswap or Aave uses $10 million of treasury funds to buy back its own token, even though it reduces the circulating supply, it also reduces the “book value” of the protocol’s treasury by an equivalent amount. Essentially, the protocol moved from a safe asset like stablecoins, to a more riskier asset (its own token) and depleted its own war-chest: capital that could have been used for development, marketing or other operations, and essentially discounted the protocol’s future growth prospects. Because of this, the market should re-price the token to reflect this reduced capitalization, neutralizing the impact of any supply shock.

Emissions vs Buyback Myth

A core reason why buybacks fail to support price is that they are insignificant compared to the sell pressure from incentives and vesting schedules. Most crypto projects operate with aggressive inflationary schedules to incentivize liquidity, users and developers.

For example, Jupiter implemented a buyback program to utilize 50% of the DEX swap fees to buy JUP tokens. They managed to buyback just 0.33%, while the emissions were 55.97%. The buyback pressure was a drop in the ocean compared to the billions of tokens unlocked for the team and the early investors.

Jupiter recently made the drastic move to halt all token emissions and cancel its planned airdrops. Extreme? Maybe. But it highlights a simple truth: you can’t fill a tank if the faucet is still running wide open.

Buying the Top

Most protocols utilize a "fee-switch" mechanism where a percentage of trading fees is automatically routed to buybacks. In a bull market, trading volumes soar, and protocol revenue hits all-time highs. The automated buyback mechanism executes its largest purchases exactly when the token price is at its peak. Conversely, in a bear market, trading activity dries up, revenue plummets, and the buyback mechanism scales down or stops entirely, exactly when the token is undervalued and the buyback would have the most impact.

Data from Messari confirms that buyback programs often execute heavily above the Simple Moving Average, destroying treasury value. For example, Aave’s buyback in 2025 spent over $15M purchasing tokens at an avg price of $223, only to see the price stagnate or drop, resulting in an unrealized loss for the DAO. By automated buybacks, protocols systematically mis-allocate capital, burning millions at the top of the cycle and providing zero support at the bottom.

The Exit Liquidity Trap

One of the most overlooked aspects of buybacks is who is actually on the other side of the trade. In many cases, protocol revenue acts as a buffer used to provide exit liquidity for investors and the team. Instead of the revenue being reinvested into the ecosystem to build new features or attract new users, it is used to "buy out" early investors, allowing them to exit their positions without crashing the price as severely.

What actually could work?

Every dollar spent on a buyback is a dollar not spent on growth. In the hyper-competitive space of web3 where new protocols launch every few days, capital efficiency is the king.

A few structural changes would put these funds to a meaningful use, rather than these hollow buyback programs.

Liquidity Provision: Instead of burning tokens in millions, the protocol could use it as Protocol Owned Liquidity (POL). This earns trading fees in revenue for the protocol and also deepens liquidity.

Yield Generation: Placing the earned revenue into yield bearing sources such as staking or lending markets creates a recurring revenue stream that compounds over time.

Research and Development: The same funds could be used to fund a world-class engineering team for years to build new innovative products.

The obsession with token buybacks is a symptom for a larger problem: the desire for a shortcut to value accrual. The data is very clear, token buybacks are not a money printer for token price.

A token’s value should come not from how much of it can be bought and burned, but from how much utility it delivers. Buybacks are a shortcut, but shortcuts rarely lead to sustainable value.

Enjoyed the read? A quick like or share goes a long way in helping more people discover it

Check out my previous article on Crypto Wallets for more insights: